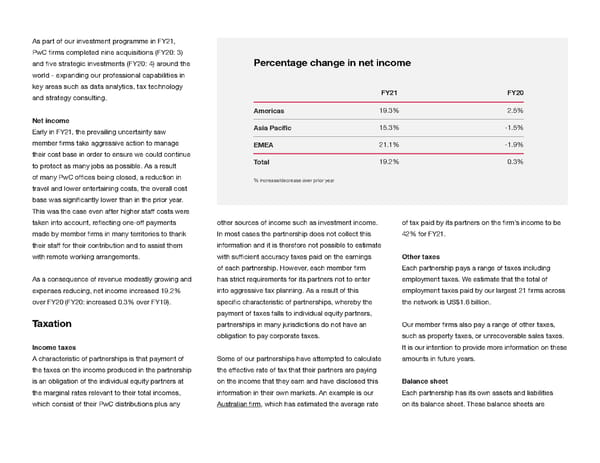

As part of our investment programme in FY21, PwC ifrms completed nine acquisitions (FY20: 3) and ifve strategic investments (FY20: 4) around the Percentage change in net income world - expanding our professional capabilities in key areas such as data analytics, tax technology and strategy consulting. FY21 FY20 Americas 19.3% 2.5% Net income Early in FY21, the prevailing uncertainty saw Asia Paciifc 15.3% -1.5% member ifrms take aggressive action to manage EMEA 21.1% -1.9% their cost base in order to ensure we could continue to protect as many jobs as possible. As a result Total 19.2% 0.3% of many PwC ofifces being closed, a reduction in % increase/decrease over prior year travel and lower entertaining costs, the overall cost base was signiifcantly lower than in the prior year. This was the case even after higher staff costs were taken into account, relfecting one-off payments other sources of income such as investment income. of tax paid by its partners on the ifrm’s income to be made by member ifrms in many territories to thank In most cases the partnership does not collect this 42% for FY21. their staff for their contribution and to assist them information and it is therefore not possible to estimate with remote working arrangements. with sufifcient accuracy taxes paid on the earnings Other taxes of each partnership. However, each member ifrm Each partnership pays a range of taxes including As a consequence of revenue modestly growing and has strict requirements for its partners not to enter employment taxes. We estimate that the total of expenses reducing, net income increased 19.2% into aggressive tax planning. As a result of this employment taxes paid by our largest 21 ifrms across over FY20 (FY20: increased 0.3% over FY19). speciifc characteristic of partnerships, whereby the the network is US$1.6 billion. payment of taxes falls to individual equity partners, Taxation partnerships in many jurisdictions do not have an Our member ifrms also pay a range of other taxes, obligation to pay corporate taxes. such as property taxes, or unrecoverable sales taxes. Income taxes It is our intention to provide more information on these A characteristic of partnerships is that payment of Some of our partnerships have attempted to calculate amounts in future years. the taxes on the income produced in the partnership the effective rate of tax that their partners are paying is an obligation of the individual equity partners at on the income that they earn and have disclosed this Balance sheet the marginal rates relevant to their total incomes, information in their own markets. An example is our Each partnership has its own assets and liabilities which consist of their PwC distributions plus any Australian ifrm, which has estimated the average rate on its balance sheet. These balance sheets are

Global Annual Review | PwC Page 12 Page 14

Global Annual Review | PwC Page 12 Page 14