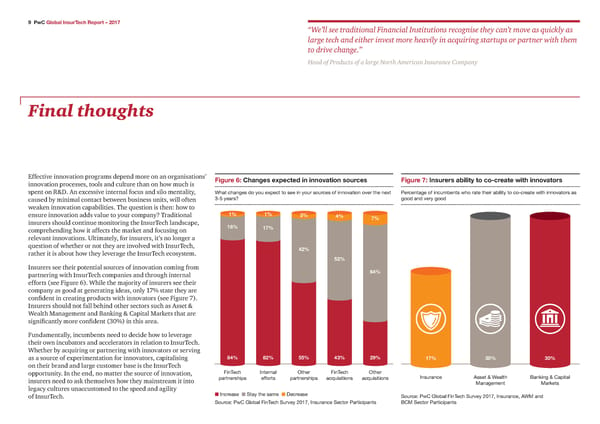

… PwC Global InsurTech Report – 2017 “We’ll see traditional Financial Institutions recognise they can’t move as quickly as large tech and either invest more heavily in acquiring startups or partner with them to drive change.” Head of Products of a large North American Insurance Company Final thoughts Effective innovation programs depend more on an organisations’ Figure Changes e„pecte‚ in innoation sources Figure 7 Insurers abilit† to co‡create with innoators innovation processes, tools and culture than on how much is spent on R&D. An excessive internal focus and silo mentality, What changes do you expect to see in your sources of innovation over the next ƒercentage of incumbents who rate their ability to co”create with innovators as caused by minimal contact between business units, will often •”™ years? good and very good weaken innovation capabilities. The question is then: how to ensure innovation adds value to your company? Traditional 1 1 3 4 7 insurers should continue monitoring the InsurTech landscape, 1 comprehending how it affects the market and focusing on 17 relevant innovations. Ultimately, for insurers, it’s no longer a question of whether or not they are involved with InsurTech, 42 rather it is about how they leverage the InsurTech ecosystem. €2 Insurers see their potential sources of innovation coming from 4 partnering with InsurTech companies and through internal efforts (see Figure 6). While the majority of insurers see their company as good at generating ideas, only 17% state they are confident in creating products with innovators (see Figure 7). Insurers should not fall behind other sectors such as Asset & Wealth Management and Banking & Capital Markets that are significantly more confident (30%) in this area. Fundamentally, incumbents need to decide how to leverage their own incubators and accelerators in relation to InsurTech. Whether by acquiring or partnering with innovators or serving as a source of experimentation for innovators, capitalising 4 2 €€ 43 2… 17 30 30 on their brand and large customer base is the InsurTech opportunity. In the end, no matter the source of innovation, FinTech ˆnternal ¡ther FinTech ¡ther insurers need to ask themselves how they mainstream it into partnerships efforts partnerships ac“uisitions ac“uisitions ˆnsurance ›sset ¢ Wealth œanking ¢ „apital ‘anagement ‘arkets legacy cultures unaccustomed to the speed and agility of InsurTech. n ˆncrease n €tay the same n Šecrease €ource‚ ƒw„ …lobal FinTech €urvey †‡ ˆnsurance‡ ›W‘ and €ource‚ ƒw„ …lobal FinTech €urvey †‡ ˆnsurance €ector ƒarticipants œ„‘ €ector ƒarticipants

Global InsurTech Report – 2017 Page 8 Page 10

Global InsurTech Report – 2017 Page 8 Page 10